Customers walked away while they waited

Confirming eligibility meant routing files to the credit desk, turning a two-minute conversation into a one- to two-day wait. This was long enough for borrowers to apply elsewhere.

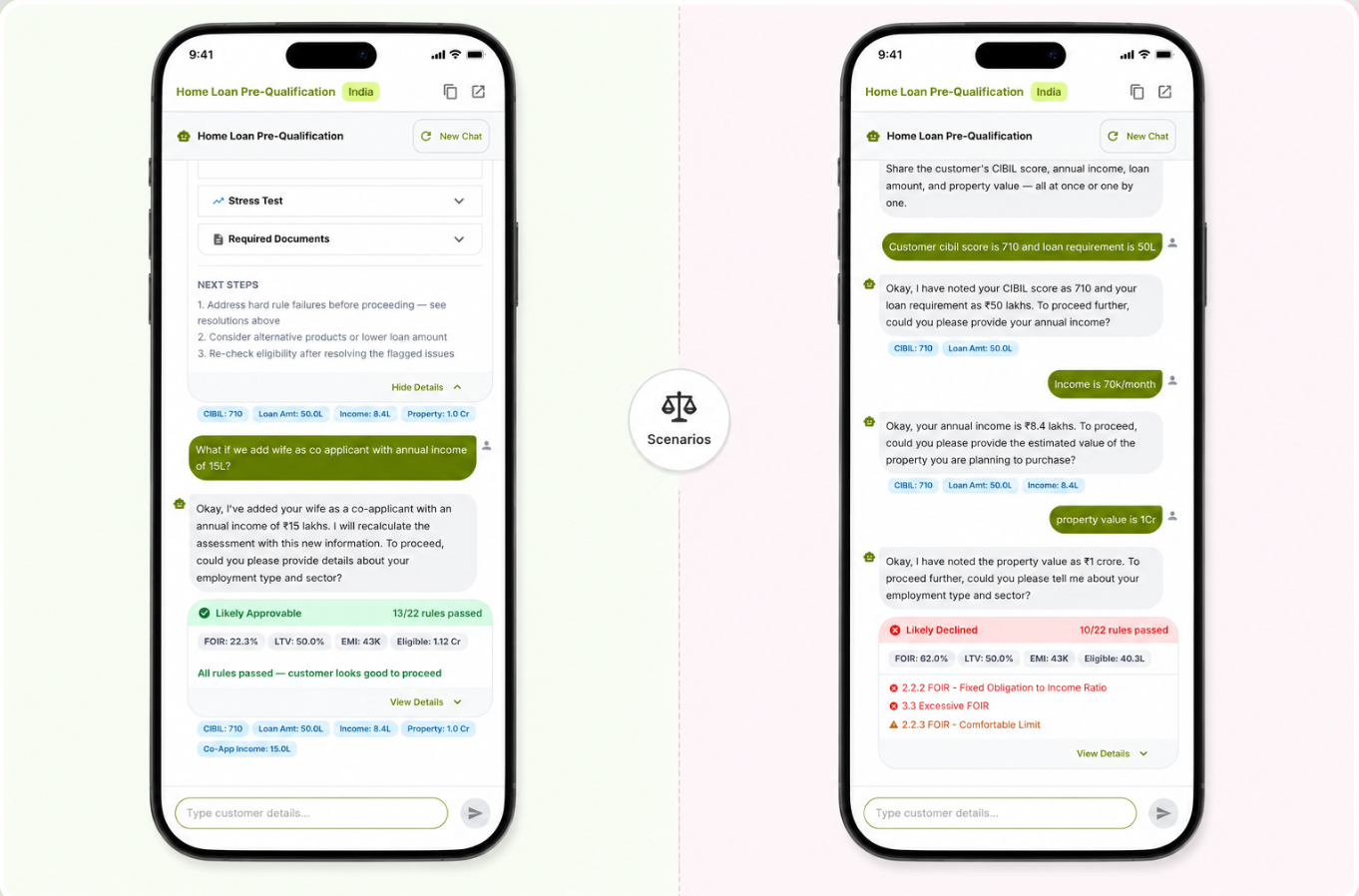

Four details in, a clear soft-signal status out in seconds

Rate, tenure, and income shocks surfaced upfront

A documented decision packet goes to the underwriter for the final call

About the client

Our customer is a mid-sized NBFC distributing home loans across India through its branch staff and a wide network of direct sales agents (DSAs). Steady growth built a strong frontline, but sales conversations consistently outpaced credit operations. Leadership wanted every borrower to get a fast, honest read at the very first meeting, without ever taking the lending decision out of human hands.

The Challenge

Confirming eligibility meant routing files to the credit desk, turning a two-minute conversation into a one- to two-day wait. This was long enough for borrowers to apply elsewhere.

Out-of-policy applications traveled all the way to underwriting before being declined, burning time meant for viable borrowers.

Outcomes and reasons varied from officer to officer, which was a weak position in a fair-lending review.

Risk and compliance would not delegate approval to opaque software. Earlier AI lending initiatives stalled before the pilot.

How Gyde solved it

Credit score, income, loan amount, property value, and within seconds, a clear status plus eligible amount, FOIR figures, LTV, and the exact documents to collect.

Every detail (employment type, existing EMIs, tenure, co-applicant income) refines the read so it's in plain language the borrower can follow.

Affordability risks, such as higher rates, shorter tenures, and a dip in income, are visible up front, so nobody is surprised later.

One tap produces the full eligibility maths, every policy rule passed or flagged, stress-test results, and a recommendation, plus a plain-language version for the borrower.

Decisions run on the lender's own configurable policy and are saved with their reasons. The system structures and explains; people decide.

The outcome

A 1–2 day wait for an eligibility answer

An honest read in the first meeting

~2 minutes to a first answer

Out-of-policy files burning underwriting hours

Non-viable files filtered at the front line

70% fewer reaching underwriting

Bankable borrowers applying elsewhere while they waited

More viable files moving forward

+18% progressed to next stage

Agent hours lost to files that could never close

Time redirected to viable borrowers

4–6 hours saved per agent, weekly

Behind the scenes

Every read runs on the NBFC's configurable underwriting policy (consistent file to file & region to region).

Risk and compliance can reopen and defend any decision long after the fact and this is a strong position in a fair-lending review.

The soft signal structures and explains; a human underwriter always makes the final call.

Explore more success stories

If you're an NBFC or bank running home loans through DSAs, we can show you exactly how the soft signal works on your policy, with your numbers.